Roughly half of the nephrologists practicing in the United States participate in Medicare’s Chronic Kidney Care Contracting (CKCC) value-based payment model. With CKCC, CMS took a major step forward in partnering with nephrologists to improve the cost and quality of kidney care.

But participating providers face unexpected financial losses this year. CMS will retrospectively adjust the benchmarks used to measure their performance. And when the goal posts move, providers may suddenly find themselves needing to retrench and even lay off staff.

So what can nephrology practices do to reduce their financial risk? One option is to move to a lower-risk, lower-reward CKCC option. Another is to scale up fee-for-service programs that benefit patients while also providing sorely-needed revenue to cushion potential CKCC losses.

We’ll explain:

Nephrology groups have access to a range of FFS programs that can provide a financial buffer for CKCC downside, protect and fund staff, and enable additional investment in programs that fuel CKCC performance.

A Whitepaper

Which fee-for-service programs can help your practice fund the transition to value-based care, while building the operational and clinical muscles you’ll need for success?

Chronic Kidney Disease (CKD) and End-Stage Renal Disease (ESRD) are seemingly excellent targets for value-based payment models: they affect large numbers of patients and have an outsized impact on the total cost of care in the U.S.

Beneficiaries with ESRD represent only 1% of Medicare patients but drive 7% of Medicare spending – and chronic kidney disease (CKD) is also a financial challenge. In 2020, 25% of Medicare fee-for-service (FFS) beneficiaries had a CKD diagnosis. Treating patients with CKD cost Medicare more than $120 billion in 2017. This is unsustainable.

Treatments for later-stage CKD and ESRD are also relatively contained within a kidney care ecosystem overseen by nephrologists. With the right support and a well-designed funding model, nephrology practices could theoretically leverage the tools available under value-based care to slow the progression of kidney disease and reduce total cost of care.

The Comprehensive Kidney Care Contracting (CKCC) model covers some Medicare beneficiaries with ESRD and CKD Stage 4 and 5. Like other value-based models, CKCC provides financial incentives for kidney care providers to reduce the cost and improve the quality of care. Ultimately, the hope is to delay the start of dialysis and prevent the need for transplant.

“The patient is a key component of the Model design. The tendency now is for patients with kidney disease to follow the most expensive path, with little prevention of disease progression and an unplanned start to in-center hemodialysis treatment. By increasing education and understanding of the kidney disease process, aligned beneficiaries may be better prepared to actively participate in shared decision making for their care.”

Nephrology groups formed Kidney Contracting Entities, or KCEs, to participate in CKCC. These KCEs could comprise just nephrologists, nephrology practices, and transplant providers, but they might also include dialysis facilities and other providers and suppliers.

However, the shift to value required a shift in thinking. Like most specialists, nephrology providers weren’t central to the initial Accountable Care Organizations (ACOs) that were launched in 2012 with the passage of the Affordable Care Act. CMS did launch the Comprehensive ESRD Care (CEC) model in 2015, which introduced ESRD Seamless Care Organizations (ESCOs) – but the focus was on dialysis providers.

To provide holistic care for all attributed patients rather than just E/M visits, nephrology practices needed new clinical and operational workflows and services. For independent practices, this may have required a significant upfront investment of time, resources, and capital.

Many partnered with entities like Interwell Health and Evergreen to help them launch and run their value-based programs, and some leveraged fee-for-service care programs that helped them build (and fund) the organizational capabilities required for success in value-based care.

Value-based payment models typically evaluate provider performance in 1-year increments, called “performance years”. In each performance year, the provider’s ability to improve quality and decrease cost is measured against a pre-established benchmark.

For CKCC, the first Performance Year (PY) ran from January 1st, 2022 through December 31st, 2022. PY 2022 included 55 KCEs. The following year, the number of participating KCEs nearly doubled. We are currently in PY 2024, and 100 KCEs are participating. CKCC currently covers 5,512 aligned nephrology providers from 516 nephrology practices – roughly half of all U.S. nephrology providers.

Participating KCEs receive adjusted capitation payments for aligned beneficiaries, are responsible for total cost and quality of care, and have the opportunity to share in savings. They can participate at different risk levels.

Not only are more nephrology practices participating in CKCC, but they are also shifting toward riskier models with higher potential rewards and higher potential losses.

KCE CKCC Participation by Performance Year

| CKCC Risk Option | Description | PY 2022 | PY 2023 | PY 2024 |

|---|---|---|---|---|

|

Graduated Level 1 |

Start upside-only, with limited potential for shared savings. Incrementally increase risk and opportunity. |

4 |

0 |

0 |

|

Graduated Level 2 |

7 |

13 |

4 |

|

|

Professional |

Earn 50% of shared savings or responsible for 50% of losses |

37 |

56 |

65 |

|

Global |

Earn 100% of shared savings or responsible for 100% of losses |

7 |

31 |

31 |

|

Total KCEs

|

55 |

100 |

100 |

|

Most value-based payment models try to predict the expected cost of care for a given population. This prediction then determines how much money providers will receive for the care of that population (typically in the form of risk-adjusted capitation payments). It also becomes the benchmark used to measure how well providers have managed the cost of care.

However, actual healthcare expenditures may be significantly higher or lower than the predicted benchmark – which can negatively impact either providers or CMS. If the benchmark was set too high, CMS pays providers much more than market conditions warrant. And if the benchmark was set too low, providers have little hope of achieving shared savings.

CMS uses a mechanism called the Retrospective Trend Adjustment (RTA) to adjust the benchmark based on actual healthcare expenditures. The RTA compares predicted and actual costs over a performance period.

Participating nephrologists are working under budgets set over a year ago – but CMS is about to make retrospective adjustments based on reference populations in each market area. CMS shared projected RTA changes with KCEs this spring.

When they received their adjusted benchmarks, a number of KCEs suddenly faced the prospect of financial losses in PY 2024. Many were concerned that the retrospective adjustment was based on historical expenditure data from the COVID era – where many healthcare consumption patterns significantly deviated from the norm.

“While nephrologists were comfortably aware of the use of the retroactive trend adjustment when entering into CKCC contracts, surprise arose over the magnitude of the reductions,” Keith A. Bellovich, DO, RPA president, told Healio. “These assumptions, using data from years when COVID skewed kidney care utilization, were completely unexpected and two to three times larger than anticipated.”

One consequence could be staffing reductions – but with most medical groups already challenged by the labor shortage, forced headcount reductions would only further impact care delivery to patients.

CMS offered KCEs two options, with a decision due at the end of April 2024.

We’re waiting to see how many KCEs decided to move to the Professional option or terminate program participation. Either way, headcount reductions and subsequent care disruptions loom – unless fee-for-service programs can help bridge the funding gap.

CKCC is just the beginning; CMS will continue to push nephrology groups toward value-based models. By leveraging currently-available FFS funding opportunities now, nephrology groups in KCEs can cushion potential losses while continuing to build out the capabilities they will need for future value-based success. (And for nephrology groups exiting CKCC, CCM can ease the transition.)

Implementing the right mix of fee-for-service programs can provide a sustainable monthly revenue stream while enhancing patient care. Often, these programs offer practices the opportunity to be fairly compensated for the high-quality care they are already providing their patients – i.e. not new work.

There are a range of FFS programs that may make sense for organizations investing in VBC – especially at scale.

ANNUAL REVENUE POTENTIAL ($ in Thousands)

| Program | Per 1,000 patients | At scale |

|---|---|---|

|

Chronic Care Management |

220 |

2,690 |

|

Transitional Care Management (CKD) |

10 |

80 |

|

Transitional Care Management (ESRD) |

150 |

440 |

|

Advanced Care Planning |

40 |

70 |

|

Kidney Disease Education |

150 |

770 |

|

Annual Wellness Visit |

30 |

240 |

At scale: Revenue potential for a larger nephrology practice running a CCM program across about 30% of Traditional Medicare and Medicare Advantage patients.

To prioritize program investments, you need to understand the potential benefits (patient care quality improvement, assistance with value-based care transition, and potential revenue opportunities) as well as the volume of patients who would qualify for the program based on payer and condition.

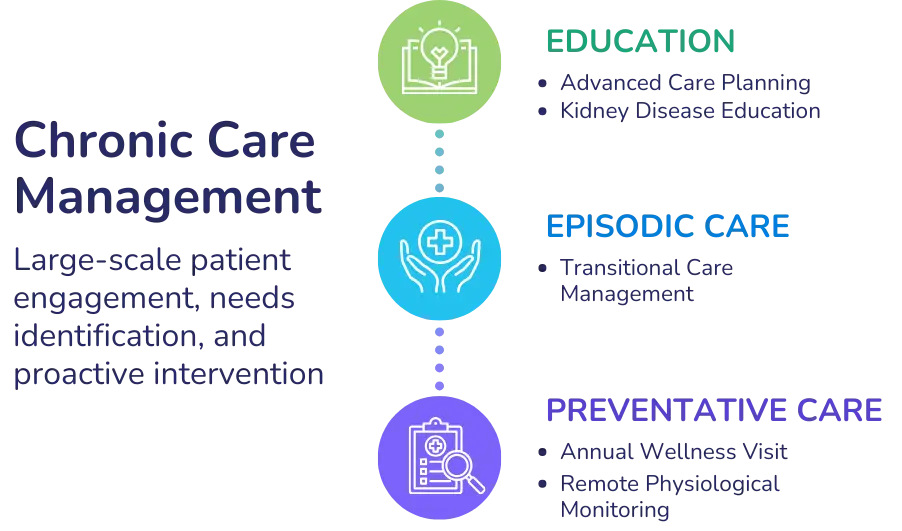

We believe that Chronic Care Management can serve as a foundation to enable other programs. CCM is fundamental; it delivers effective, proactive patient engagement at scale. With the insights you gain from your CCM program, you can identify which patients may have other needs and direct them to the appropriate programs. And because you have created a trusted relationship with those patients through CCM, they are more likely to engage in those programs and ultimately see better outcomes.

We walk through different options – from Chronic Care Management (CCM) through Kidney Disease Education (KDE) in our newest whitepaper.

A Whitepaper

Which fee-for-service programs can help your practice fund the transition to value-based care, while building the operational and clinical muscles you’ll need for success?

Darshan has 15+ years experience co-founding and building high growth healthcare technology businesses committed to improving access to care and quality of care. More about Darshan…

Alyssa believes that solving between-visit care is critical to effective population health management and long-term success under value-based models. For over a decade, she has worked with innovative health systems, large medical groups, and payers across the United States to help them implement programs and share their successes under advanced payment models.

Phamily © 2025. All Rights Reserved.